|

|||||||||

|

|

| 2025 China's technical textiles industry performance and 2026 outlook |

|

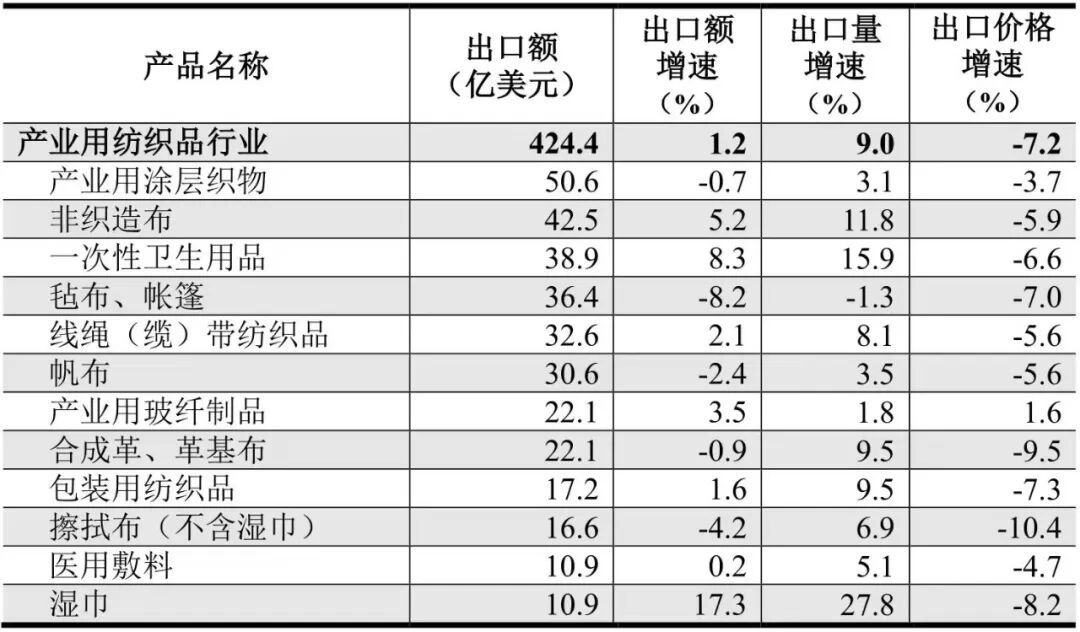

Economic performance in 2025 In 2025, the global economy faced a fragile recovery amid persistent tariff shocks, trade uncertainty, rising protectionism, and geopolitical tensions. Against this challenging backdrop, China's economy demonstrated resilience, maintaining steady progress with positive momentum and structural upgrading. China's technical textiles industry responded nimbly to external pressures and intensifying competition, accelerating transformation to sustain positive development. 1. The production maintains medium-high growth Domestic and export demand for China's technical textiles steadily recovered in 2025. Markets such as wipes, automotive components, and wind power grew over 10%. Environmental protection and infrastructure sectors saw stable demand, while hygiene materials accelerated toward high-end, differentiated development. Key end-markets provided solid support for high-quality industry growth. Capacity utilization remained healthy overall, especially in H2 when the industry's production index was in rapid expansion. Full-year output of major products maintained mid-high growth. China Nonwovens & Industrial Textiles Association (CNITA) surveys show sample enterprises posted 73.5% capacity utilization for 2025, with about 36% exceeding 80%. According to CNITA statistics, China's technical textiles fiber processing volume reached 22.796 million tons in 2025, up 6.6% year-on-year. Nonwoven fabric production reached 9.207 million tons, up 7.5% year-on-year. 2. Profitability improves with sharp divergences across segments According to the National Bureau of Statistics (NBS), revenue and total profit of above-scale enterprises in technical textiles fell 2.4% and 7.0% year-on-year, respectively. Gross "> Figure 1 Operating profit rate of enterprises above designated size in China's industrial textile industry (unit:%) Source: NBS, CNITA According to the data of the National Bureau of Statistics, the main economic indicators in each sub-field in 2025 are as follows (see Table 1): Nonwovens: Revenue -1.7%, profit -7.1%; gross gross gross gross gross strap products (US$3.26 billion, +2.1%), fiberglass technical products (US$2.21 billion, +3.5%), packaging textiles (US$1.72 billion, +1.6%), and felt/tents (US$3.64 billion, -8.2%). Nonwoven roll exports surged 11.8% in volume (1.694 million tons) and 5.2% in value (US$4.25 billion). Disposable hygiene products (diapers, sanitary napkins, etc.) grew 8.3% to US$3.89 billion, wet wipes continued double-digit growth for three consecutive years to US$1.09 billion, while protective garments (including medical) and masks reached US$780 million and US$610 million, respectively.

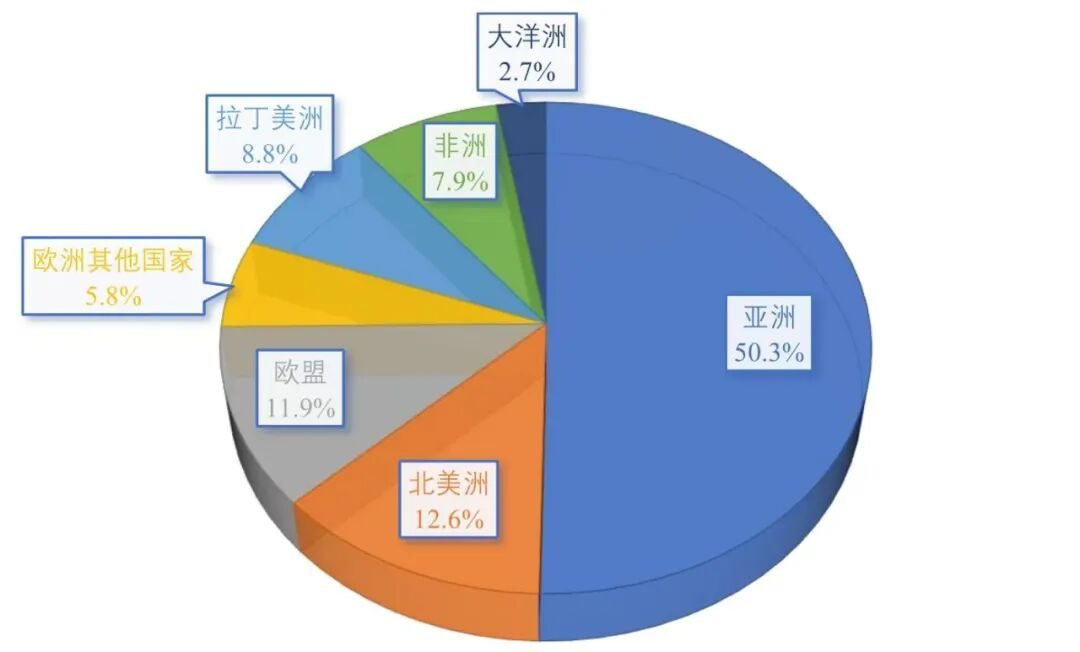

Table 2 Export situation of China's industrial textile industry and main products in 2025 Source: NBS, CNITA Export markets: Asia accounted for 50.3% of total exports (+1.5% year-on-year). Exports to North America fell 8.9%, while those to the EU grew 3.8%, Latin America 5.3%, and Africa 11.6% (largest share increase). Exports to Oceania fell 1.2%.

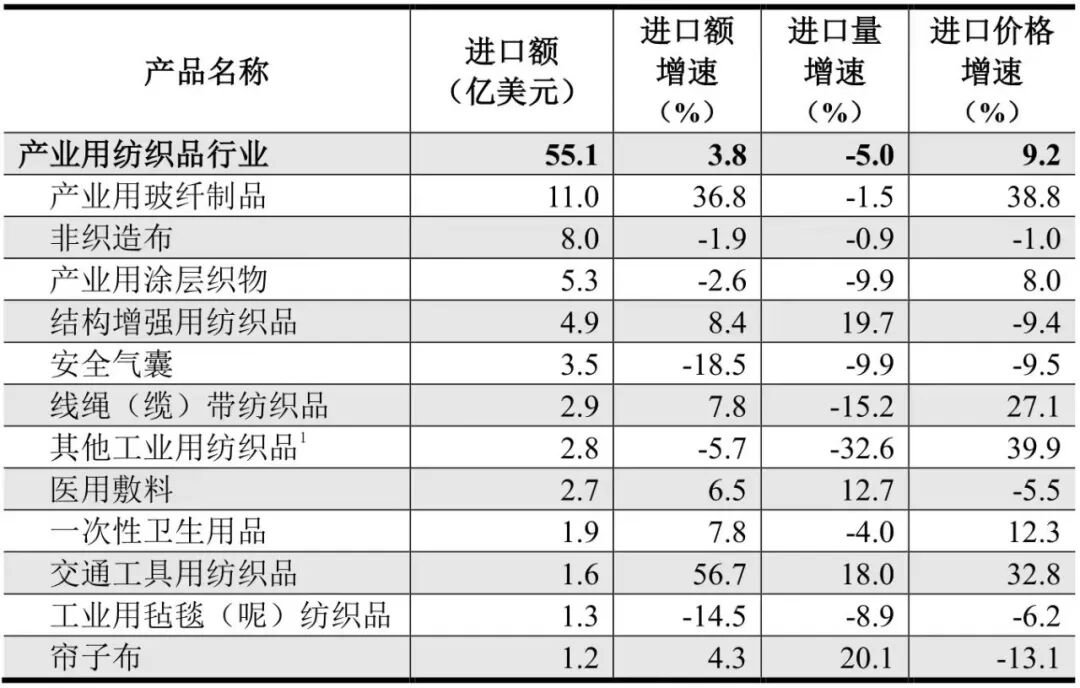

Figure 2 Main export areas of China's industrial textiles in 2025 Source: China Customs, CNITA Imports: Technical textiles imports reached US$5.51 billion in 2025, up 3.8% y-o-y (first positive growth since 2021). Major categories: fiberglass technical products (import value +36.8%, price +38.8%), structural reinforcement textiles (+8.4%), cordage & strap products (+7.8%), nonwovens (-1.9% to US$800 million), coated technical textiles (-2.6%), and airbags (-18.5%). Table 3 Import situation of China's industrial textile industry and main products in 2025

Note: Other industrial textiles mainly include PMP hollow fiber membranes, specially coated fabrics, filter materials, polishing materials for semiconductor industry and other industrial fabrics. Source: China Customs, CNITA 2026 Outlook 2026 is the inaugural year of China's 15th Five-Year Plan and a critical juncture for China's modernization and industrial transformation. The technical textiles industry faces both strategic opportunities and risks. External environment: Global economic recovery remains fragile amid persistent shocks. Escalating geopolitical conflicts, rising trade protectionism, and regional supply chain restructuring continue to generate uncertainty and instability. The recent Iran-Israel conflict not only worsens regional geopolitical instability but also disrupts global oil supply and international shipping systems—posing challenges to China's exports of technical textiles, including rising trade barriers, increasing competition from emerging market peers, narrowing price 's high-quality development during the 15th Five-Year Plan. New industrialization and building China into a manufacturing powerhouse will drive high-end demand in new energy, infrastructure, biomedical, and aerospace sectors, helping resolve structural supply-demand imbalances. Effectiveness of policy support for technological innovation, green and low-carbon transition, and private sector development will accelerate digital and green transformation, driving business model shifts from scale expansion to quality and efficiency improvement, reinforcing the industry's full-chain advantages, and enhancing resilience and global competitiveness. Industry development: China's technical textiles industry is in a recovery phase overall—operating loads remain high and profitability improved. However, growth momentum needs strengthening, structural supply-demand issues persist, and challenges such as continued product price declines and profit lagging revenue in certain segments remain to be addressed. Over the long term, the industry's advantages—complete supply chain, continuously iterating technological innovation, and the strategic support of a massive domestic market—will become more prominent, strengthening resilience and risk-bearing capacity. Forecast for 2026: China's technical textiles industry is expected to maintain stable operations, with major economic indicators achieving low-to-mid growth and development quality and efficiency continuing to improve. Fixed asset investment will continue focusing on equipment upgrades, digital transformation, and green manufacturing, while capacity expansion investments will remain cautious. |